Future Outlook on Automotive Electronic with Rising Opportunity for Taiwan

2020/03/16 | By CENSThe Scale of Global Automotive Electronics

The global automotive electronics market size reached US$ 267.6 billion in 2018 and is expected to hit US$ 355 billion by 2023, with a CAGR of 5.6%, according to Strategy Analytics. The current output value is mainly driven by driving information systems, connected cars, and autonomous driving assistance systems (ADAS).

")

The Status of Taiwan’s ICT industry

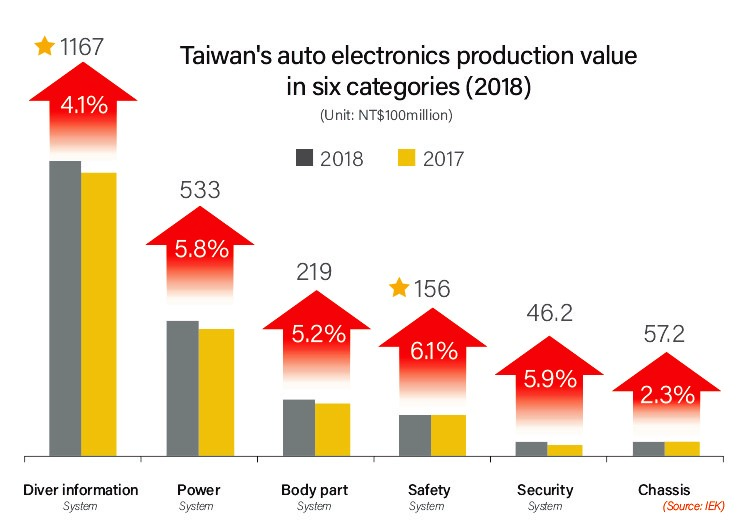

Taiwanese auto electronics market was valued at NT$ 220.2 billion with a growth of 5.6% in 2018. Due to the rise of the Smart Vehicle Systems and Internet of Vehicle (IOV), we can see a 4.1% rise in the related application of driving information system and hardware of IOV with the value reaching NT$ 116.7 billion. In terms of safety systems, since European and North American regions have actively been rolling out vehicle safety regulation, new cars equipped with Automatic Emergency Braking (AEB), Lane Departure Warning System (LDWS), and Driver Monitoring System (DMS) will become mandatory by international regulations in the future.

The huge business potential makes it the new battleground. However, entering the automotive field is not an easy task. Automotive systems still are subject to many strict and complex inspections to ensure the safety of pedestrians and drivers. Besides, since car longevity is at least up to a decade, manufacturers must also offer a long warranty period.

In response to the above needs, many manufacturers have launched a variety of products and services, which target automotive electronics. Manufacturers can also use this to quickly design a framework that meets automotive standards, enhance product competitiveness, tap into the supply chain in the automotive industry, and grasp the forthcoming and tremendous opportunities in automotive electronics.

The Rise of Taiwanese Automotive Electronics Supply Chains

Among the supply chains benefiting from the development of smart cars and electric vehicles in Taiwan, five major automotive electronics supply chains are forecasted to benefit, including battery materials, automotive lenses, automotive semiconductors, automotive electronic parts, and connected cars. The most invaluable component for electric vehicles is the battery. Taiwanese manufacturers provide related chemical materials to international battery factories such as Panasonic, Samsung, and LG. For example, Coremax and Mechema are the top two oxidation catalyst factories in Taiwan, providing metals such as cobalt and nickel for power batteries in Panasonic electronics. The key to the future of smart cars lies in the integrated use of four core technologies - automotive lenses, sensors, radar, and optical radar. Among them, automobile lenses manufactured by Asia Optical has entered the Tesla supply chain, while Calin Technology, a pioneering auto-lens supplier in Taiwan, is now supplying Lidar and Waymo. TSMC has also begun to layout for automotive semiconductor needs, announcing that it will construct a new 8-inch wafer fab in Taiwan to meet the demand for sensors and MCU (microcontroller unit) and MOSFET (metal oxide semiconductor field effect transistor) wafers. International automotive giants have launched a variety of smart cars and electric vehicles. The construction of various new component supply chains has sprung up. Taiwan already has a solid foundation in the automotive component supply chain with vigorous R&D in the ICT industry and competitive quality and technology in automotive parts production. With manufacturers leveraging their ability into smart vehicles and vehicles cars, the business opportunities of automotive electronic parts are emerging with full potential.

Taiwan ICT Industry to Set Foot in New Niches

ICT industry taps in the field of connected car and electric car with handful resources, for instance Delta Group enters automotive electronics with OE electronic control system and audiovisual system. By taking advantage of AU Optronics's panel advantages and wireless communications, BenQ entered the market through the driving information system, while panels conglomerates- Innolux Corporation and AU Optronics—are actively engaged in automotive electronics. Despite the challenges, the benefits are clear as products maintain high gross profit and high-added value.

Taiwan's automotive electronics products are mostly used in navigation, multimedia and vehicle imaging. Autonomous vehicles and connected vehicles will promote advanced driving safety assistance systems, such as automotive imaging systems, blind spot detection, lane shifting, parking assistance systems, and products for LEDs automotive lighting solutions. Both autonomous and connected vehicle sectors are expected to exceed NT$ 270 billion in 2020. Taiwan's automotive electronics products, however, still focus on producing a single part component, and are usually second-tier suppliers. In order to qualify as a first-tier supplier, they must cultivate the ability to integrate and intelligent capabilities, thus enhance their competitiveness in line with international auto plants.

Source: Automotive Research & Testing Center / Industrial Technology Research Institute")